Before we start, I must clarify I mention Vanguard a lot. That’s just because they are the platform I use and I am familiar with them. The method below should work with other platforms too and I heard it works with Fidelity as well. Anyway, back to our main topic- how to “increase” your ISA allowance using fees.

Just over a week ago, I received a new message from Vanguard. I use Vanguard to manage my ISA (individual savings account). It was just a letter telling me my fees are due but it included a very interesting piece of information I wasn’t aware of.

First, let me make sure we understand the terms ISA. If you know what an ISA is and understand it, please skip the “What is an ISA?” section.

What is an ISA?

As per Google’s dictionary, an ISA is “a scheme allowing individuals to hold cash, shares, and unit trusts free of tax on dividends, interest, and capital gains.”

This is a UK specific account. Its definition means that any compound interest or yield will be available completely tax-free.

“So why doesn’t everyone hold all of their investments in an ISA?”

Ah, if only that was possible. There is a limit on how much you can contribute (pay in) to an ISA in a tax year, for the tax year ending April 2021 that amount is £20,000 per person. That means that you can not contribute more than £20,000 but if that amount grows to £20,000,000 (yes, 20 million) you will be able to pull it all out with no capital gain taxes.

Realising my ISA allowance can go further

Back to Vanguard’s message. They told me my fees are due and also included the following text:

“We’re writing to let you know that your Vanguard account fee is due. You don’t have to do anything as we will sell some of your investments to cover the amount and we don’t charge for this service.

If you’d prefer us not to do this, you can add cash to your account within 6 business days of receiving this message. We’ve given you some details on how to do this in this email.”

And later in the message, I read this little gem:

“For all future payments, you can have your fees debited directly from your bank account if you wish.”

This was followed by instructions on how to do so, which I’ll explain shortly. First, I want to explain why the way you pay your fees is important.

Why does the payment method matter?

Example

Let’s take two people, FI person and Lazy FI person. Both are very responsible with money and both are fortunate enough to have more than £20,000 a year to invest.

Both characters invest £20,000 with Vanguard at the beginning of every tax. They both have more than that to invest each year, let’s say £25,000.

They both invest all their ISA allowance in the same fund, let’s say it returns 5% a year.

There is one difference between them. FI person pays the annual 0.15% platform fee from the ISA balance (cash, if there’s any, or investments). This is the default setting. Lazy FI person, on the other hand, pays it via direct debit.

Year 1

They both pay £20,000 to an ISA which will be worth £21,000 at year-end with 5%. Let’s say the average balance was £20,500 (average of £20,000 and £21,000). This means the fees for year 1 will be £30.75 (£20,500 * 0.15%) because fees are paid on the average balance.

FI person pays it from the ISA. He now has £20,969.25 (£21,000 – £30.75) in his ISA, he then invests £5,000 in a non-tax-advantaged account.

Total investments- £25,969.25

Lazy FI person pays it using direct debit. He is left with the full £21,000 in his ISA and then invests £4,969.25 (£5,000 – £30.75)in a non-tax-advantaged account.

Total investments- £25,969.25

I can go on to years 2 and 3 and show you that as time goes by and your balance grows, the difference will become bigger. However, we’re both lazy and the point is already clear (I hope).

The key message:

While you will end up with the same total balance, paying your fees via direct debit means a larger % of your investments are in your ISA and the gains there will not be taxed. This can save you a lot of money when you do decide to sell part or all of your Investments. It also helps you assume a 0% tax rate at retirement.

Although in the first year it is only £30.75, after a decade you will probably reach Vanguard’s capped fee of £375 annually if your investments perform well. This means that instead of £19,625 growing tax-free, the full £20,000 can grow tax-free!

Do I want a bigger portion of my investments (up to £375 a year) growing tax-free? You bet I do.

Is it worth spending 2 minutes and setting up a direct debit? Absolutely, the only reason I can think of not doing it is if you literally invest all the money you can afford to and you need every other penny for your monthly living expenses. If you can think of another reason to not pay via direct debit, please let me know in the comment section.

So how do you actually do it?

As mentioned, I use Vanguard so will explain (step by step) how to do it on their platform but it should be pretty similar on other platforms. I included screenshots from their desktop site, the mobile website should be just as easy to follow.

“Increase” your ISA allowance using fees- step 1

on the left-hand menu, click on “My profile”.

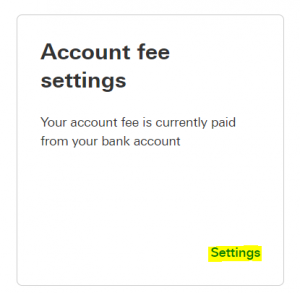

“Increase” your ISA allowance using fees- step 2

If you haven’t done so already, you need to give them your bank details to set up the direct debit. You will see 2 rows of 3 boxes each, click on “Settings” in the box titled “Account fee settings”, it is the middle one in the 2nd row.

You will see 2 rows of 3 boxes each, click on “Settings” in the box titled “Bank account”, it is the left one in the 2nd row.

Then insert your bank details and click “save”

“Increase” your ISA allowance using fees- step 3

Repeat step 1, You will see 2 rows of 3 boxes each, click on “Settings” in the box titled “Account fee settings”, it is the middle one in the 2nd row.

“Increase” your ISA allowance using fees- step 4

Choose the option titled “Pay from my bank account” and click “save”.

“Increase” your ISA allowance using fees- step 5

Enjoy your “increased” ISA allowance. I hope this can help you reach FI quicker.

Set up once and enjoy the benefit forever, ideal laziness.

Dear Lazy Dad!

Thanks for teaching me a new thing today! It makes perfect sense when you think about it. Id like to email you about a podcast episode for my own venture if thats alright. Let me know if this is something you are interested in.

Alex.

Always happy to share knowledge and I’m happy you learned something.

You can email me at LazyFIDad@Gmail.com (can you believe this was not taken?) and we can discuss further.

Hi,

Have a look at this link, I think it can help save more by using the tax relief.

It’s vanguard related so hopefully should help.

https://monevator.com/sipp-money-saving/?fbclid=IwAR2yQLSBhlxpduRwbuTfPgEgmOXFBw2PUvoyr0ZQG1Y-2PwRg-0qxRtcJo8#comment-1339592

Really interesting about paying your fees from your account if not maxing out your allowance, I see what he means and never thought about it.

I think I’ll get pretty close to maxing it next year but definitely an interesting concept and I’ll keep it in mind, thanks for sharing!