This post is going to be super-niche. It will be completely irrelevant for most of you. For the few of you that this is relevant for, you can save £100s off your NI (National insurance) payments with very little effort. I’m going to explain how you can save a big chunk of your NI payments using your pension contributions (but not increasing them).

Who is this relevant for?

This is only relevant for you if you:

- Earn more than £4,189 a month/ £50,268 a year gross (before tax)

- Have an employer that allows you to easily change your pension contributions each month

- Have a pension that is “salary sacrifice”

Background

I attended the Financial independence London Meetup*. The meetup itself was interesting but when it ended, some people stayed on to chat. One of those people was Duane. Duane is a fellow FI pursuer and a fellow mystery diner.

Duane shared with us an awesome hack he found to save money on NI with pension contributions. I’ll do my best to explain how it works, the advantages, and the disadvantages.

I am almost embarrassed to admit how excited I was to find out about this.

Before we go any further, we need a disclaimer:

I am not a tax adviser and don’t know your personal situation. This content is not tax advice and should not be treated as tax advice. Please do your own research and/or use a tax professional before acting.

How NI is calculated

Income tax

I don’t know if you know that but Income tax is calculated annually. That means that if you had a high salary for 6 months and was then unemployed for 6 months, you’ll probably get money back as you paid higher tax while employed. That’s because while you were employed, it was assumed you’ll earn that amount each month for a full year (12 months). When the tax year ends, HMRC looks at how much you earned for the year and recalculates your tax, this could result in a refund or an additional charge.

NI

National insurance is a different story. It is calculated for each pay period, this can be weekly, monthly, or annually.

The downside of this calculation method is you will not get a refund if you’re unemployed for part of the year. Your allowance or calculation resets after each paycheck you get.

The upside of this calculation method is that we can use this periodic reset to save some big money. We can do this by timing our pension contributions, I’ll explain the mechanics shortly. I can’t believe I never thought of that and that this is not common knowledge, thanks Duane for pointing this out!

Assuming you get paid monthly:

The first £797 you earn each month are exempt from national insurance.

Anything you earn between £797 and £4,189 each month is taxed at 12% (NI only, income tax is separate).

Anything above £4,189 a month is taxed at 2% (Again- NI only, income tax is separate).

Example 1- £72k a year, no bonus (flat pension contribution rate)

Let’s get to know Lazy FI person 1:

- Lazy FI person 1 earns £72k a year (£6k a month) and has no bonus.

- His employer offers a pension contribution match of up to 5%. Lazy FI person 1 knows employer matches are awesome and will always contribute at least 5% of his base salary to his pension.

- Lazy FI person is a dad and wants to get his taxable salary down to £50k to get the full child benefit.

He does some quick maths and realizes he needs to contribute £22k a year to his pension. He calculates a contribution rate of 31% (22/72 rounded up).

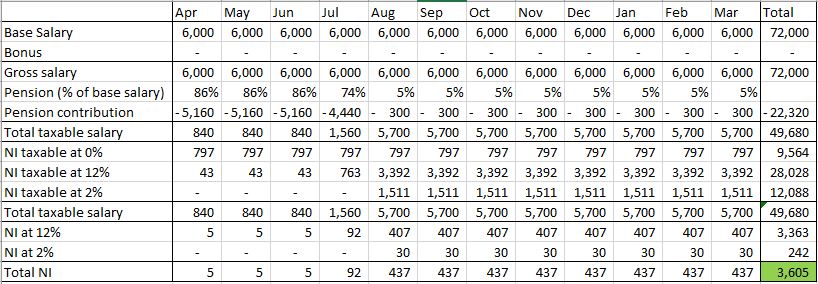

Here is how his NI calculation looks like:

How to read this

The Uk tax year starts on April 6th each year and ends on April 5th the following year. That’s why my months are from April until March.

The first line is the base salary.

The second line is the bonus (no bonus in this example)

Then we have the Total (base salary + bonus)

The pension contributions were calculated above at 31% to get us under £50k annual.

This sums to a monthly contribution of £1,860 but more importantly- £22,320 a year. This figure will be important in example 2.

Once you deduct the pension contributions from the Total (third line) you get your taxable salary. We see £49,680, just under £50k.

The next section shows the split of each salary into the NI tax rates.

Then we see a breakdown (and total) of the NI charge. Total NI- £4,814.

Important things to notice in example 1

Notice how £40.1k out of the £49.7k is taxed at 12%? we’re going to fix that.

Also, remember his gross salary (£72k), his total pension contributions (£22,320), and his total NI charge (£4,814). Let’s see how we can reduce that.

Example 2- £72k a year, no bonus (custom contribution rate)

Same details as before but this time, Lazy FI person 1 tries to save NI with pension contributions. He will still contribute the same amount annually but will spread it out differently.

Key principles:

Lazy FI person 1 will not reduce his taxable income below £797 a month. He wants to utilise his NI exempt amount.

On the other hand, he will also not contribute less than 5%, he does not want to lose his employer match.

Method

Lazy FI person 1 does some quick maths again. He notices that to get to £797 (in a specific month), he needs to contribute 86% (1 – 797/6000, rounded down so we don’t lose NI exempt money).

He contributes 86% for the first 3 months (April-June) and 5% for the last 8 months (August-March). That leaves him with 74% in the fourth month (July) in order to have the same contributions as in example 1.

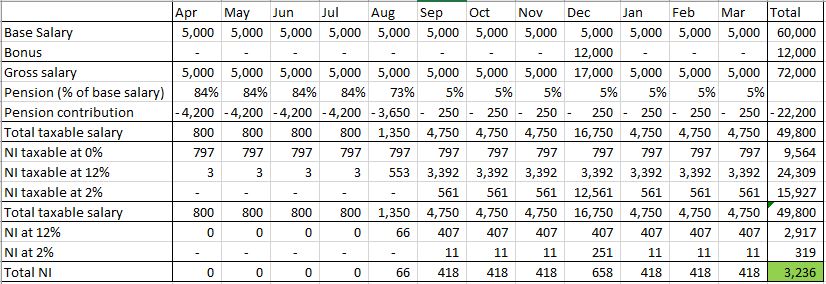

Here is how his NI calculation looks like:

Important things to notice in example 2

In this example, Lazy FI person 1’s gross salary (£72k) and pension contributions (£22,320) are the same as in example 1.

Remember how £40.1k out of the £49.7k was taxed at 12% in example 1? Look at him now. He moved £12.1k to the 2% rate.

Look at the total NI charge! it’s down from £4,814 to £3,605! That’s a saving of £1,209!

You can see where the £1,209 comes from. We transferred £12,088 from a 12% rate to a 2% rate, saving 10%.

£12,088 * 10% = £1,209 (rounded to the nearest pound).

Look how much he was able to save on NI with pension contributions, my mind is blown.

I feel like NI handed me an amazing tax hack!

Example 3- £60k a year, 12k bonus (flat contribution rate)

Let’s get to know Lazy FI person 2:

- Lazy FI person 2 earns a base salary of £60k a year (£5k a month) and gets a £12k bonus once a year, in December.

- His employer also offers a pension contribution match of up to 5%. Lazy FI person 2 also knows employer matches are awesome and will always contribute at least 5% of his base salary to his pension.

- Lazy FI person is also a dad (shocking, I know) and he also wants to get his taxable salary down to £50k to get the full child benefit.

He also does some quick maths and realizes he needs to contribute £22k a year to his pension. He calculates a contribution rate of 37% (22/60 rounded up). This assumes the pension contributions are calculated on the base salary only.

Here is how his NI calculation looks like:

Important things to notice in example 3

Because of the bonus in December, Lazy FI person 2 has one month with a big salary. A big chunk of it (£11k) is charged at 2%, that’s good! That’s why his total NI charge (£3,732) is lower than Lazy FI person’s NI charge in example 1 (£4,814).

Also, remember his gross salary (£72k), his total pension contributions (£22,200), and his total NI charge (£3,732). Let’s see how we can reduce that.

Example 4- £60k a year, 12k bonus (custom contribution rate, the right way)

Same details as in example 3 but this time, Lazy FI person 2 tries to save NI with pension contributions. He will still contribute the same amount annually but will spread it out differently. He does it the right way (we will see in example 5 what the wrong way is).

Key principles:

Just like Lazy FI person 1, Lazy FI person 2 will also not reduce his taxable income below £797 a month. He also wants to utilise his NI exempt amount.

On the other hand, he will also not contribute less than 5%, he does not want to lose his employer match. Just like Lazy FI person 1.

Method

Lazy FI person 2 also does some quick maths again. He notices that to get to £797 in a specific month, he needs to contribute 84% (1 – 797/5000, rounded down so we don’t lose NI exempt money).

He contributes 84% for the first 4 months (April- July) and 5% for the last 7 months (September-March). That leaves him with 73% in the fifth month (August) in order to have the same contributions as in example 1.

Here is how his NI calculation looks like:

Important things to notice in example 4

In this example, Lazy FI person 2’s gross salary (£72k) and pension contributions (£22,200) are the same as in example 3.

Remember how “only” £10,961 out of the £49,800k was taxed at 2% in example 3? Lazy FI person managed to increase that to £15,927. That’s an additional £4,966, not bad!

Look at the total NI charge, it’s down from £3,732 to £3,236. That’s a saving of £496!

Just like in example 2, the £496 is the 10% saving (from 12% to 2%) on the £4,966 he moved to the 2% bracket.

The savings in this example (£496) is smaller than in example 2 (£1,209) because there is a high salary (December, due to the bonus) which already had a chunk in the 2% bracket, even in example 3, where Lazy FI person 3 used a flat rate.

In April-August in the table above we have £3 each month taxed at 12%, the “NI at 12% row” shows zero due to rounding.

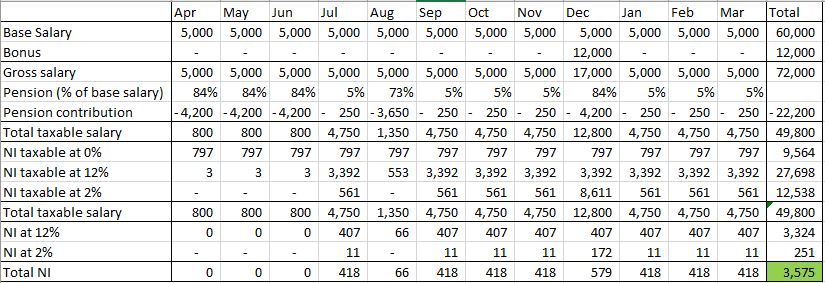

Example 5- £60k a year, 12k bonus (custom contribution rate, the wrong way)

OK, one more example.

Lazy FI person 2 understood how moving the majority of pension contributions to fewer months can save him money. However, he tried to be too smart for his own good. He thought to himself:

“I know I’m getting a huge salary in December, I don’t need all that money. Let me contribute 84% in that month (instead of 5%) and in return, I’ll lower July’s contributions from 84% to 5%”

Let’s see what happens:

Important things to notice in example 5

How come his total NI charge go from £3,236 to £3,575? That’s an extra charge of £339!

The reason we save NI with pension contributions is that we want some months to have the highest taxable salary possible. That way, we get a bigger percentage of our salary taxed at 2% rather than at 12%. Lazy FI person 2 had one big salary in the year, that’s exactly the month to leave it to be as high as possible! contribute the minimum to max the employer match, that’s it.

This is my favourite example because that’s what I planned to do when I first heard about this “hack”. I’m so happy I ran the numbers, could’ve cost me a few £100s.

Save NI with pension contributions – Summary

Using these 5 examples, we showed that save NI with pension contributions. All we have to do is move from a flat percentage to a variable (custom) percentage.

We also saw that in the highest paying months- we should contribute the least to our pensions.

Things to consider before you save NI with pension contributions

The model

- I frontloaded the pension to contribution for simplicity, you don’t have to. You can move the months around as long as you don’t increase the pension contributions in the months with the highest gross salary. For example, in example 2 we did 3 months of 84%, one month of 74%, followed by 8 months of 5%. You can do one month of 84% then 2 months of 5% and repeat this for 3 quarters. In the final quarter, have one month of 74% followed by 2 months of 5%. You’ll get the exact same result.

- This method means you will have a few months with a higher net (after-tax) pay and a few months with lower net pay. If this fluctuation makes you feel uneasy, you don’t have to use this method, that’s fine. It requires some cashflow planning and isn’t for everyone.

- Want to play around with the numbers? Be my guest, here is the file I made while trying to get my head around this concept. I included 5 tabs, one for each example. You can access the file by clicking here. I restricted the access to view only (for obvious reasons). If you want to change the numbers, feel free to download a copy to your computer.

Your circumstances and tax considerations

- If you are about to apply for a loan/mortgage soon, having a few salaries with a low net pay may affect your loan/mortgage. In that case, delay the higher contributions to after you get accepted for the loan/mortgage.

- If you are a high earner, the pension contribution limits (currently £40k a year with some caveats) may make things a bit harder for you.

- In order to implement this method, you must earn more than £4,189 a month/ £50,268 a year. Otherwise, you don’t reach the 2% (soon to be 3.25%, see below) bracket.

- From tax year 22/23 (starting April 6th 2023), the NI rates will increase by 1.25%. 12% will change to 13.25% and 2% will change to 3.25%. This method should work exactly the same, you will still save 10% on any amount transferred to the lower rate bracket. However, the total charge will be higher due to this increase. You can read about the increase in this GOV.UK page. You can also see the rates and brackets on that page.

- This method might mess your tax code a bit. However, as I mentioned in the beginning, if you are overcharged, you’ll get refunded by HMRC. You can also get an extra charge so please do your own calculations and/or use a tax professional.

- My employer allows me to change my contribution percentage with a click of a mouse button. Some employers don’t. Some employers force you to choose your percentage once a year. My old employer allowed me to change it but I had to ask payroll to do it each time. They would hate my guts! Is the relationship with the payroll team worth more or less than the amount saved? That’s for you to decide.

Notes

* This happens almost every month, feel free to join:

Link to the meetup page

One final note:

I only found out about this on Tuesday (16/11/2021). This post is a result of my journey to understand this concept. If I got anything wrong, please let me know by commenting on this post. We are all here to learn 🙂

Important update

As John Kash mentioned in the comments, I missed something in the examples above. There is a limit on how low you can get your net salary.

Based on the GOV.UK guidance:

“A salary sacrifice arrangement must not reduce an employee’s cash earnings below the National Minimum Wage (NMW) rates. Employers must put procedures in place to cap salary sacrifice deduction and ensure NMW rates are maintained.”

How much is the National minimum wage?

The current (21/22) rate is £8.91 an hour, going up to £9.50 in 22/23 (see the rates here) for people aged 23 or over.

That means that if your contracted hours are 35 hours a week (most office jobs from my understanding), that’s £311.85 a week (35 * £8.91), going up to £332.50 a week (35 * £9.50) from 22/23. If we multiply this by 52 we get to £16,216.20 a year, going up to £17,290. The final step is dividing by 12 to get the monthly NMW:

£1,351.35 in 21/22, going up to £1,440.83 from 22/23.

Apparently, you can not get your net salary below that amount using salary sacrifice.

I may have missed a few pounds here or there, happy to be correct.

Thanks again John for pointing this out, I love it when readers teach me new things.

Important update number 2

I misunderstood how the NMW threshold is calculated and it cost me hundreds of pounds. Please read this post to avoid making the same mistake:

Lazy FI Dad, I love your posts, your energy and your amazing understanding of UK financial system and our language even though you are Israeli.

Congratulations on the baby expectancy news.

Keep up the great work, Claire

Thank you for your kind words. I was definitely very excited when I wrote this post. It’s crazy to think that by timing my pension contributions differently, I can save hundreds of pounds.

I will be implementing this in the upcoming tax year and once it’s over, will update here. This will be a year and a half from now though 🙂

Actually, thinking as I type, there are still 4 paychecks left this year (I think it’s too late for November), I’ll see if I can do a mini version in these 4 months.

You cant reduce your salary below minimum wage in any pay period with salary sacrifice. £840 is below that.

You typically cant change the amount sacrificed often with many company salary sacrifice schemes. I believe the HMRC rules changed on minimum frequency but employers haven’t necessarily changed their systems or want the overhead of constantly changing contracts.

Thanks John,

1. Are you sure about 840? I thought you’re allowed to contribute 100%. I am no tax expert so will look into it and update the post, thanks for pointing this out!

2. Agreed, I mentioned this at the beginning of the post in the “Who is this relevant for?” section.

Hi Again John,

Thank you so much for pointing this out, I added 2 more sections at the end of the post and (of course) gave you credit.

Salary Sacrifice creates a temporary new contract between you and your employer where they pay you less and they pay the sacrificed amount directly (you can see this in your pension transactions where it shows as an employer contribution). Hence as a contract of employment they can’t pay you less than NMW.

I note that the employer also saves 13.8% employer NI on the deal.

The fact it is your new contractual salary can be an issue when applying for mortgages.

Makes sense about the new contract although you can change that any time, can’t you?

Regarding mortgage- I 100% agree, see the first items in the “Your circumstances and tax considerations” section where I addressed that.

Regarding the employer’s savings- I didn’t address that for 2 reasons:

1. I only care about my (and your) savings haha, this post is more for employees, not employers

2. Companies are not eager to share these savings with you. Although, some do.

Another point is you cant just average it by dividing it by 12. Some months can have 23 weekdays/working days. You have to be paid minimum wage for all the hours/days you worked in the month. John Lewis was named and shamed for averaging and accidentally paying below minimum wage in some months.

Dude, this is just entirely and utterly incorrect.

NI is taken on gross, not net (i.e. after income tax).

I agree 100%, can you point me to where I said otherwise?

Example 2, row 11 – where you state taxable pay is net when it would be the gross (6000).

Your mobile is entirely and absolutely incorrect.

I read example 2 again and can’t see where I mentioned that NI is charged on net salary, sorry. I absolutely agree with you that NI is taken on gross (before income tax) but after pension (salary sacrifice). That means you can reduce or increase your NI (and income tax but that’s not the topic of the post) by contributing more or less to your pension.

Also, I want to thank you for taking the time to read the post and leave the comment, it makes the content better. Once I see which sentence (or is it the whole post?) I got wrong, I’ll gladly correct it. Just like I did with the NMW from John’s comment.

NI is absolutely NOT calculated after pension is removed. The entire premise of this article is wrong.

Your understanding of gross and net is also wrong. Gross is before any deductions. Adjusted net income is the pay you’re left with after pension deductions. Net pay is after all tax and the calculated NI payment.

The calculation of NI is on the full gross pay, i.e. before any pension deductions.

Sorry but no cigar.

Haha, I like “no cigar”, haven’t heard that before.

When you say “NI is absolutely NOT calculated after pension is removed.”

and

“The calculation of NI is on the full gross pay, i.e. before any pension deductions.”

you are, unfortunately, wrong and misleading when talking about salary sacrifice pensions (the topic of this post).

However, just saying “you’re wrong” is not enough and doesn’t automatically mean I’m right.

Therefore, I went and looked for “proof” for you and for anyone else reading this, because I think this “debate” (couldn’t think of a better word) can be really helpful for other readers.

Please go to this link:

https://www.gov.uk/guidance/salary-sacrifice-and-the-effects-on-paye

I hope we can both agree that the GOV.UK (HMRC) have their facts straight and know their own tax rules.

Now, please scroll to the title “Examples of salary sacrifice”.

Let’s look at example number 3.

It has an employee receiving a bonus of £5,000 with all of it being sacrificed towards a pension.

If you’re right, that person will have to pay NI (and income tax) on that 5,000.

If I’m right- they won’t.

Let’s see what GOV.UK (HMRC) has to say:

“No employment income tax or National Insurance contributions charge to the employee – the full amount is invested in the pension fund.”

You can also go to this link (although not as official as a GOV.UK website):

https://thepeoplespension.co.uk/salary-sacrifice/

It says “Using salary sacrifice means that the employee and the employer pay less National Insurance contributions.” (first sentence in the 3rd paragraph).

Now that I responded to that part of your comment, let me address the other part.

You say: “Your understanding of gross and net is also wrong. Gross is before any deductions.”

Again, I agree with the 2nd part, gross is before any deductions, you’re correct. Where did I say anything else?

You’ve misunderstood the HMRC guidance. They mean whatever you sacrifice goes in full (i.e I pay 5k in, precisely 5k ends up with my pension provider) and you do not pay income tax on that 5k. NI however is calculated on gross so you still pay full stamp.

Your excel clearly shows the incorrect application of the HMRC rules.

Don’t worry, you are 100% correct that when salary sacrifice is in place NI is calculated after pension contribution.

Hi, I can see what Steve is saying above. Basically, in the Excel you’re calculating the NI based on a post-pension taxable income. This doesn’t work here because NI is calculated by your gross / initial income so sacrificing more in some months is irrelevant for NI purposes. Annoying as I thought the above was ingenuous on first glance!

Hi Liam,

Thanks for reading and taking the time to comment.

I’ve looked into it by speaking to a tax accountant and double checking my payslils.

Apparently, it’s up to the employer where they put the NI. My employer (and my 2 previous ones, all big corporations) all calculated taxable income (for both income tax and NI) AFTER pension contributions (salary sacrifices). After speaking to several people and a tax accountant, I found out some employers put it in a diffent section in the payslil which means that for them, this tip/hack is irrelevant.

It may be irrelevant for you and Steve (sorry) but it definitely works for some. Once the tax year is over, I’ll share an update. My payslip conventionally has a “NIable salary YTD” section and total NI for the year. It will ve very easy for me to calculate how much it would be if spread even. Aiming to post this mid April.

Thanks for the post, I was certainly similarly excited when I read it.

My employer has salary sacrifice.

My full salary is known as a “Reference Salary”.

Pension contributions are selected by me and are monthly adjustable through salary sacrifice. This percentage adjusts my actual salary, i.e. Gross. i.e. I met the criteria you set out at the start.

On my payslip “Salary” is the smaller post-sacrifice amount. Tax and NI are deducted based upon this value. HMRC do not get told what my “Reference Salary” is, so cannot treat it as gross, only the post salary sacrifice “Salary” number. Therefore, I believe the method proposed would work in my situation.

However, I’m not brave enough to trial it yet for 3 reasons – inconvenient cashflow, the modest (but not immaterial!) relative potential saving, and medium confidence it’ll work.

Thanks again for the post, really interesting!

No worries, I’m trialling it for you haha. I’ll post an update around mid-April.

For your 3 reasons:

1. I agree with the inconsistent cash flow. We don’t mind it too much.

2. The “modest” saving is subjective and as it’s free money and an interesting experiment- I’m trying it.

3. My experiment can save you experimenting yourself, just wait 3-4 months and I’ll post an update.

Salary Sacrifice gives you a temporary new contract of employment with lower salary, and the employer contributes the sacrificed amount directly. Hence the sacrificed amount is never part of your earnings so there is no NI or tax to pay.

https://monevator.com/salary-sacrifice/

Thanks! Very interesting read.

I think, regarding the live discussion this post has created, the key message is:

“The upside is you do not pay tax or National Insurance Contributions (NICs) on your foregone salary.”

Been on salary sacrifice for over 20 years, big fan of it and it’s been a game changer for me in the last few years, my yearly salary/bonus is in the mid £40k area, my dividends from general investments have been getting high enough that they could push me into the higher tax bracket but using salary sacrifice I can manage a buffer to be tax efficient with my dividends. A £10,000 dividend has a tax rate £750 instead of £3,250 managing it this way.

One year though I did get my calulations wrong and drift a few £100 into, not a big deal but now I don’t try managing it so close the tax bracket freshholds, just have a large buffer going into the pension via SS leaving a consistent monthly net salary, if I’m short then I’ll just draw on the dividend investment income rather than the reinvesting it. In a few years it may make sense to sacrifice me more closer to the minimum wage and make more use of dividend income to support more of the living expenses.

For me income tax & NI are both calculated against the salary sacrifice amount (pension contribution already taken out), my employer will also uplift my bonus by 10% if I salary sacrifice it into my pension, I keep asking them to consider doing the same on the salary element as well.

That’s incredible!

Yes, employers also save their own NI if you contribute more to your SS but it’s very rare that they share that saving with the employees, bravo to your employer.

£10k in dividends is outstanding! If you don’t mind me asking, is it from investing in dividend stocks or paying yourself from a business you own?

Handful of dividend paying shares. 80% comes from a single share, a long term bet which is on the right path on the dividend side but has a longer upside to go on the growth side. Most of the rest comes from a previous company share schemes where the dividends get reinvested automatically and it’s snowballed to match a couple of months net salary each year. This represents 50% of my pot, rest are DC / DB pensions with DC eliment all in index funds. I’ve got the time, patience and at some point the individual shares will be sold and proceeds put into index funds to reduce the volitility of drawdown.

Hi…

This is an interesting read. I’ve been committed to maximising money efficiencies for 8+ years. So am very open to innovative opportunities.

I raise this by way of context as I see no reason not to maximise financial returns in all/any forms. But I do wonder if there is a limit to such action.

Cliche alert: apologies in advance but… where would we be if everyone that could adopted the approach outlined here?

Is there a limit to maximising one’s own returns – a point at which the greater collective win to society is lost?

NICs are a tax for better or worse that brings benefits to all (no matter how inefficiently). As we’ve learnt during the paying for care crisis, it turns out that NICs is not hypothecated to state pensions but simply added to wider tax pot. Ho hum… that’s life…

I have had a decent job paying more than decent money, I’ve inherited a good sum (in part as a result of caring for the later life circumstances of both parents and my uncle)… and I have a DB pension.

My money savvy ensured that I could fund my parents’ care fees through renting their property, claiming allowances and managing their savings, which they in turn had cultivated precisely for the expensive last years of their life.

I can’t help thinking that money-wise energy and expertise is better directed at these big ticket items of financial security rather than playing the table to reduce my NICs contribution to wider pot and wellbeing.

Here endeth the lesson… now shoot me down in flames. I’d be interested to hear people’s thoughts.

Chris

Chris

Hi Chris, no shooting down in flames, only a simple disagreement, which I love, as that’s how we all learn 🙂

You took the time to not only read what I wrote but even leave a comment and I appreciate that.

First of all, sounds like you’ve done really well for yourself, well done!

If I understand your points (please tell me if I didn’t), you’re saying:

1. Tax is going to good (although inefficiently) places and as a society, we should not try to reduce it too much.

2. It’s not enough money for the hassle

Let me respond to each point separately:

1. This is more of an ethical question so I’ll try and answer it as one.

As I explained in the post, income tax is calculated annually while NI is not. If you get fired from your job halfway into the year, you might get a tax refund for paying too much income tax, with NI that doesn’t happen! For most people, the fact that NI is calculated weekly/monthly is bad. All I’m doing here is showing a little benefit to this mainly-bad system.

This is for this “hack” specifically.

Regarding tax as a wider concept, I see it as my duty (yes, my duty) to pay as little tax as possible (legally of course). I will never agree with everything the government does, why not keep as much money as you can and, if you choose to, donate it to your cause to align it to your values?

Another thing, which you mentioned when you said “NICs are a tax for better or worse that brings benefits to all (no matter how inefficiently).” I think that the brackets are crucial here! I wonder how much of your tax goes to these inefficiencies (I don’t know the answer) but I’m sure having someone check and process the benefits of those in need costs a lot of money in salaries. Public money is usually very inefficiently used, I’d rather keep as much of it as I can and use it according to my own values.

Where would be as a society if we all behaved this way? I think that in a much better place. If people take more responsibility for their lives (financial aspect included), there will be fewer people on benefits and the tax money can be better used. If more people take care of themselves financially, the money will go to those who really can’t do any better.

I hope this makes sense.

2. I ran the numbers and for the tax year 22/23 (April 22- April 23), it should get us a few extra hundred pounds. Is it worth it?

2.1 Yes! It’s literally just moving pension contributions from one paycheck to the other, it’s free money.

2.2 I agree it’s a bit of a hassle to change these, run the calculations and deal with the cash flow fluctuations but Lazy FI Mum is ok with that, we did a cash flow plan for the year and, most importantly, I’m just fascinated to see how accurate my calculations work, I’m a numbers person and it’s not a hassle for me, I’m genuinely fascinated by this. You can call this a hobby 🙂

2.3 When you say we should maybe focus on “bigger ticket items”, these aren’t mutually exclusive, why not do all of it?

I really hope I didn’t completely misunderstand what you meant.

Hi Lazy FI Dad…

You raise some interesting issues, which have been well worth sharing. Many thanks…

That an NI repayment on par with tax is not available is key here, perhaps?

Plus, thinking about it: anyone going self employed in later life will doubtless have no need to pay further NI as they’ll have passed limit required some time ago. In a sense, what’s the difference between that and juggling payments when PAYE.

Looking more broadly, your point about covering the big picture gains AND the micro/niche tricks is valid. I certainly try to do that – but perhaps to my disadvantage.

A mild obsession with the micro on may part (albeit not to the level of rebalancing NI) and the distractions this created may well have cost me far bigger gains in terms of further promotions at work. The ££s generated from promotion would likely have dwarfed all the credit card stoozing and bank account bribe grabbing (in addition to index investing). At its peak, overseeing this was quite an admin task.

Or may be the distraction kept me sane in my job for longer?

Looking more broadly and perhaps randomly…

With the heating cost crisis upon us, why don’t more people follow MSE Martin Lewis – and in this instance fix heating for 2-3 years in 2021, as he kept advising. The poorest are on pay-as-you-go meters but so many are not. The saving here again dwarfs so many other savings to be had.

All in all, it’s a big topic. Thank you for contributing to it…

Chris

Slightly concerning: in section 3.1.3: “If an employee is paid in irregular or unequal payments and it’s established that this avoids, or reduces, the payment of National Insurance contributions, you can be directed to work out National Insurance contributions on a different basis.”

https://www.gov.uk/government/publications/cwg2-further-guide-to-paye-and-national-insurance-contributions/2022-to-2023-employer-further-guide-to-paye-and-national-insurance-contributions

Interesting, I wonder if that refers to freelancers, shift workers or something else.

In any case, I think most people have a steady salary (full time employees) so this “hack” can be relevant for them.

I was prepared to try this NI “hack” in the 2025-26 tax year to save around £500 but this guidance makes me hesitant. As you say, Section 3.1.3 includes the key wording “or unequal payments”, which is exactly the effect of ramping up and down pension contributions as described in this article. Would HMRC notice or care for a paltry £500? Maybe not but clearly they have guidance for such situations that suggests they don’t like employees “avoiding” NI this way.

However, what would be absolutely fine according to this guidance, IMO, is to simply front-load the pension contributions. e.g. instead of switching between 0% and 60% contributions each month, you could contribute 60% for 6 months, then 0% for 6 months. That way, the payments wouldn’t be “unequal” or “irregular”, you’d have just changed your mind half way through the tax year about how much to sacrifice, which is a valid thing to do IMO and probably wouldn’t even be noticed.

The downside of course is it means you either need existing savings to eat into during those first 6 months of low take home pay, or you need to do 6 months at 0% first (or as low as will get you maximum employer matching), which means you lose out on 6 months of pension compounding.

Hi Lazy FI Dad, many thanks for sharing the examples and inspiring for the NI hack. I read your article some time ago but only now I’m back to work after maternity leave and I’m designing my pension contribution year to fall under 50k bracket and minimize the NI contributions.

I’m far away from being a tax expert and your excell snapshots are very useful in revealing the black magic on NI contributions, so big kudos for that to start with. Have you ever updated it for the 2022-2023 NI brackets (https://www.gov.uk/national-insurance-rates-letters)? If I read them correctly there is no longer 2% bracket for the income above £4,189 but only the 15.05% for above anything we earn over £758. I tried to replicate the examples and I can’t see any NI savings between the two cases a) equally splitting the pension contribution throughout the year and b) maximizing them over short period. Many thanks for your thoughts on this. PS: And congratulations for the new son that I read about in the part 2 article on this topic:)

Hi Ania, thanks for the congratulations and for your great question (why haven’t I updated the numbers):

First, I’m not sure where you got 15.05% from, the rates went up from 2% and 12% to 3.25% and 13.25%. Can you help me and point me to where 15.05% came from?

Update: just went to your link, you were looking at the “employer” section, not the “employee”, look at one table above 🙂

I have avoided updating the rates for 3 reasons:

1. It doesn’t matter, really. While they changed from 2%/12% to 3.25% to 13.25%, the savings by moving from one rate to another is still 10% so while the total NI you’ll pay will not agree to my calculators, the saving due to this method will still be the same.

2. This tax year is a bit weird, the NI thresholds change mid-year (July if I’m not mistaken).

3. Pure laziness (the negative one haha), I’ll try and update them in the near future.

However, if you want (this applies to anyone reading this), you can always email me at lazyfidad@gmail.com and ask for an unprotected version of any of my files, I’ll be happy to share them. I use protected versions to embed in my posts so no one can delete cells by mistake and ruin it for everyone else. Once you have an unprotected version, you can change any cells you want.